Citizens Property Insurance Corporation, often referred to as Citizens Home Insurance is a not-for-profit, tax-exempt government corporation created to provide insurance to Florida homeowners who cannot find coverage in the private market. It serves as a last-resort option for homeowners in Florida. Citizens Home Insurance reviews and ratings are mixed. Overall, Citizens Home Insurance is a viable option for those who cannot find affordable coverage in the private market, but it comes with certain limitations and potential drawbacks. Homeowners complain about difficult customer service, especially during the claims process and low liability coverage limits. Despite some complaints, Citizens receives stable and high ratings from insurance ranking companies like AM Best, Fitch, S&P.

Citizens has a depopulation program aimed at reducing the number of policies by encouraging policyholders to switch to private insurers when possible. Policyholders can manage their policies, make payments, access policy documents, and report and view claims online through the myPolicy portal.

Pros and Cons of Citizens Property Insurance

Citizens Property Insurance Corporation is a crucial option for Florida homeowners who cannot find affordable coverage in the private market. While it offers essential and often more affordable coverage, it comes with limitations such as fewer coverage options, coverage caps, and potential difficulties in the claims process. Policyholders should weigh these pros and cons when considering Citizens as their insurance provider.

Pros

- Availability: Provides coverage for homeowners who cannot find affordable insurance in the private market.

- Affordability: Often offers more affordable rates than private insurers, especially for high-risk properties.

- State Support: Backed by the state government, ensuring some level of stability and reliability

- Essential Coverage: Acts as a last-resort option, ensuring that homeowners have some level of protection.

- Discounts: Offers discounts for adding safety features to homes, such as hurricane shutters or alarm systems

Cons

- Limited Coverage Options: Fewer extra coverage options compared to private insurers.

- Coverage Caps: Coverage is capped for higher-value homes (e.g., homes worth more than $700,000).

- Difficult Claims Process: Many customers report challenges with the claims process, including slow response times and inadequate settlements.

- Surcharges: Policyholders may face surcharges if Citizens does not have enough funds to pay claims after major events.

- Mandatory Flood Insurance: Recent laws require Citizens policyholders to buy flood insurance, which can increase costs

- Customer Service Issues: Many customers complain about difficult customer service, especially during the claims process.

- High Denial Rates: High rate of claims denials compared to private insurers.

Citizens Property Insurance Coverages, Limits and Rates

Citizens policies, particularly older or more basic forms, may offer less comprehensive coverage or lower limits for certain items compared to policies available in the private market. For example, personal liability limits are typically lower, and coverage for items like screened enclosures or certain types of water damage might be limited or excluded.

Home Insurance rates are highly individualized. The “average rates” provided below are estimates or statewide averages based on available data (as of May 2025) and can vary dramatically based on location (county, proximity to coast), property value, construction type, roof age, desired coverage amounts, chosen deductible, mitigation features (like hurricane shutters), claims history, and other factors.

Citizens policyholders are increasingly required to obtain separate flood insurance policies, phased in based on property value. This is an additional cost separate from the Citizens premium.

Citizens Coverages and Limits

Here is a table summarizing the coverage limits and average rates for Citizens Property Insurance Corporation:

| Coverage Type | Coverage Limits |

|---|---|

| Dwelling (Coverage A) | Up to $700,000 (less than $1 million in Miami-Dade and Monroe counties) |

| Other Structures (Coverage B) | Typically 10% of Coverage A |

| Personal Property (Coverage C) | Typically 50% of Coverage A |

| Loss of Use (Coverage D) | Typically 20% of Coverage A |

| Personal Liability (Coverage E) | $100,000 standard, higher limits available |

| Medical Payments to Others (Coverage F) | $1,000 per person standard, higher limits available |

| Additional Coverages | Optional coverages such as Sinkhole Loss, Personal Property Replacement Cost, etc. |

Note: Rates are calculated only for Coverage A, namely Dwelling. When you purchase Dwelling coverage, you also purchase other B, C, D, E and F coverage.

Average Annual Premiums

Citizens’ rates are regulated. State law includes a “glide path” that limits how much rates can increase annually for existing primary residence policies, aiming to gradually bring rates closer to actuarial soundness without causing extreme shocks. For 2025 renewals, this cap is 14%. (Non-primary residences have a higher cap, up to 50%).

| Dwelling Coverage Limit | Citizens Average Premium |

|---|---|

| $150,000 | $3,699 |

| $300,000 | $7,353 |

| $350,000 | $8,529 |

| $450,000 | $10,528 |

| $750,000 | 12,063 |

Coverage Options:

- Homeowners (HO-3, HW-2): For detached, single-family homes and duplexes where at least one unit is owner-occupied. It covers the building, other structures on the property, personal property, additional living expenses, and personal liability.

- Modified Homeowners (HO-8): A restricted policy covering 11 named perils with several exclusions, including water damage.

- Dwelling Fire (DP-3, DW-2): For tenant-occupied properties and properties that may not qualify for an HO-3 or HO-8 policy. It covers the dwelling, other structures, personal property, and loss of rent or additional living expenses.

- Condominium Unit Owners (HO-6, HW-6): For condo owners, covering the unit’s interior, personal property, additional living expenses, and liability.

- Mobile and Manufactured Homes (MHO-3, MW-2): Covers mobile and manufactured homes, including the home itself, other structures, personal property, additional living expenses, and personal liability

The Florida Office of Insurance Regulation (OIR) 2025 Rate Changes

- The Florida Office of Insurance Regulation (OIR) approved rate changes effective June 1, 2025. The statewide average increase for the most common homeowners (HO-3) policies is 6.6%, and the average increase across all personal residential primary policies is 8.0%.

- However, Governor DeSantis announced projected average statewide decreases of 5.6% for 2025, highlighting significant decreases for many policyholders in South Florida (e.g., average -6.3% in Miami-Dade, -4.5% in Broward).

- Conclusion: Rate changes are complex. While the overall approved rate filing shows a modest average increase statewide, specific territories and risk factors mean many policyholders, especially in South Florida, may see decreases, while others could see increases up to the 14% cap.

Factors Influencing Your Specific Rate

- Property Location (County, ZIP code, distance to coast)

- Home Value (Dwelling Coverage Amount)

- Age and Construction of Home (Wood frame vs. concrete block)

- Roof Age and Type

- Wind Mitigation Features (e.g., shutters, roof shape, roof-to-wall connections)

- Chosen Deductibles (Higher deductible usually means lower premium)

- Policy Type (e.g., HO-3, DP-1, Condo HO-6)

- Personal Claims History

- Credit-Based Insurance Score

What is the cheapest home insurance?

Citizens Property Insurance Claims

Citizens Property Insurance Corporationreviews is mixed regarding to its claims process. Some customers appreciate the affordability and the availability of coverage when private insurers are not an option. Many customers report difficulties with the claims process, particularly after natural disasters like hurricanes. Complaints include slow response times, inadequate settlements, and poor customer service.

Citizens Property Insurance has a high rate of claims denials. In 2023, nearly 17,000 claims (about 50.4%) were denied. This rate is higher than that of private insurers, which have denial rates around 46%. Denials can be due to various reasons, including duplicate claims, invalid claims, and claims that do not meet the policyholder’s deductible. The company does not track specific reasons for each denial.

Weiss Ratings, an independent ratings agency, highlighted that Citizens has consistently had high rates of closing claims without payment over the past five years, ranging from 40.2% to 50.5%. Homeowners have expressed frustration, feeling financially strained and “ripped off” due to the high rate of claim denials

Overall, While Citizens Property Insurance Corporation provides essential coverage for homeowners who cannot find affordable insurance in the private market, its claims process has significant challenges. High denial rates and customer dissatisfaction are notable issues. Policyholders should be prepared for potential difficulties in the claims process and consider these factors when choosing their insurance provider.

How to File a Claim

Filing a claim with Citizens Property Insurance Corporation involves several steps to ensure that policyholders receive the necessary support and compensation for their losses. Here is an overview of the claims process:

- Report the Claim:

- Online: Policyholders can report and track claims through the myPolicy portal.

- Phone: Call Citizens at 866.411.2742, available 24/7.

- Initial Assessment:

- An adjuster will be assigned to evaluate the claim. The initial estimate will be based on the policy type, identification of covered damages, coverage limits, deductible amount, and repair standards adjusted for local labor and material costs.

- Documentation:

- Policyholders should provide all necessary details about the claim, including the date, time, and location of the incident. They should also submit any required documentation, such as photographs, receipts, and repair estimates.

- Emergency Measures:

- If it is safe, take reasonable emergency measures to protect the property from further damage. This may include temporary repairs to prevent additional harm.

- Initial Payment:

- For non-catastrophic claims, Citizens will issue a partial payment based on the initial estimate, less the policy deductible. For catastrophic events like hurricanes, initial payments are made based on the actual cash value of the damages.

- Supplemental Claims:

- If additional covered damages are discovered during repairs or if the contractor’s estimate is higher than the adjuster’s original estimate, policyholders can file supplemental claims.

- Final Settlement:

- As repairs are completed, Citizens will distribute additional payments to cover the replacement costs of the covered damage. Policyholders should contact Citizens before beginning repairs for damages not included in the initial estimate

Citizens Claims Additional Information

- Catastrophe Claims: Citizens has specific procedures for handling claims related to catastrophic events, ensuring quick initial payments and ongoing support throughout the repair process.

- Sinkhole Claims: There are special considerations and processes for sinkhole claims, which may involve additional inspections and evaluations.

- Insurance Fraud: Policyholders are encouraged to be aware of and report any suspected insurance fraud.

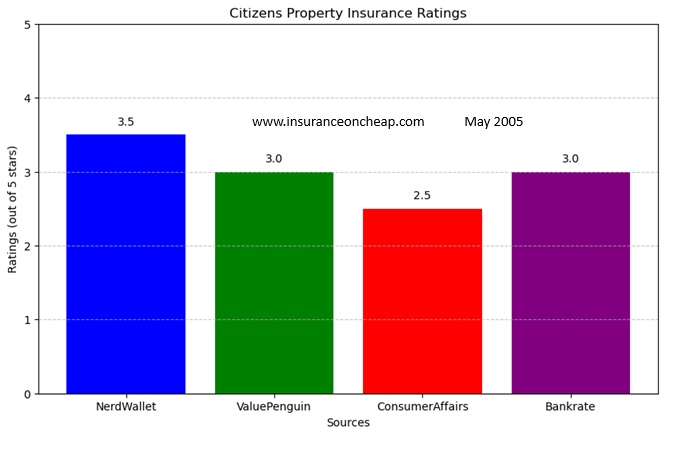

Citizens Property Insurance Reviews

Citizens Property Insurance is a vital resource for many Florida homeowners unable to secure private insurance. However, potential customers should be aware that reviews frequently highlight significant challenges, particularly with claims handling, customer service responsiveness, and relatively basic coverage limits compared to private market options. It’s often considered a “last resort” option, necessary but potentially involving trade-offs in service and coverage.

Customer reviews are generally mixed, often leaning towards negative, particularly concerning the claims process and customer service. Citizens receives a significantly higher number of complaints compared to the average insurance company of its size, according to the National Association of Insurance Commissioners (NAIC) complaint index (reported indices include 4.28 and figures indicating 3 to 4 times more complaints than expected). However, it serves a critical role by providing coverage to homeowners, especially in high-risk areas, who cannot find affordable insurance in the private market.

Common Themes in Positive Reviews

- Availability: Praised for being an option when other private insurers deny coverage or offer significantly higher premiums (policyholders may qualify if private quotes are >20% higher).

- Lifeline: Seen as a necessary safety net in Florida’s challenging insurance market.

- Affordability (Relative): While overall premiums can be high, some customers find Citizens’ rates cheaper than the limited private options available to them. Some report monthly payments being affordable.

- Specific Positive Experiences: Some customers report prompt and efficient handling of non-catastrophic claims (like interior water damage) and good customer service from agents.

- Disaster Response: Sets up catastrophe response centers for in-person support after major events.

Common Themes in Negative Reviews & Complaints

- Claims Handling: This is a major source of complaints. Issues include:

- Significant delays in processing claims and sending adjusters (especially after hurricanes).

- Difficulty contacting assigned adjusters and getting responses.

- Claim denials or disputes over the scope and cost of repairs.

- Slow payment to homeowners and contractors.

- Feeling mistreated or accused during the claims investigation process.

- Customer Service: Reports of difficulty getting answers, long wait times, lack of communication, and needing to constantly follow up. The 24-hour support line is sometimes criticized for only being able to forward messages to adjusters who may not call back promptly.

- Limited Coverage: Policies are often basic with lower coverage limits compared to private insurers (e.g., fixed $100,000 liability, low limits for valuables like jewelry, no coverage for animal liability/dog bites, often no coverage for water backup). Fewer endorsement options.

- High Premiums & Potential Surcharges: While sometimes the only option, premiums are noted as being high (potentially 2-3 times the national average) and have been increasing. There’s a risk of special assessments levied on all policyholders if Citizens’ funds are depleted after major disasters.

- Strict Underwriting: Homeowners may be required to make repairs (like removing trees, replacing fences or pipes) to maintain coverage. Eligibility criteria must be met.

- Financial Stability Concerns: Despite good financial ratings (e.g., A from A.M. Best, A from S&P), its growing exposure, underwriting losses, and reliance on potential assessments raise concerns about its capacity after major events, even prompting a federal investigation inquiry.

Last Citizens Property Insurance Reviews

Last Citizens Insurance Positive Reviews

- They’re great service protection and I’d recommend them anytime to everyone and cheap to pay every month and very beneficial to me and my family. I’m very Happy with them now and will keep them for awhile.

- Quick quote and awesome rates. Coverage vs. rate is very good. The agent has been very helpful answering all our answers and we receive our notice of changes on time.

- They are always there, ready to help and take the time to answer any and all questions you may have about anything concerning your insurance policy. In a time where people feel disconnected to each other, this company connects with its customers well.

- They are great because I have never had to use them. Always a live person on the phone and willing to help. They work well with my mortgage provider and always provide the information needed. Insurance is expensive, but they have managed to keep our rates steady over 9 years.

- We have used citizens for almost 6 years now. Although we have not had to make a claim I am very satisfied with them. The reps are always friendly and professional. As with anything our rates go up yearly. Flood insurance is reasonable also.

- StateFarm came through for me when my house got flooded from septic tank. They replaced all my carpet and fixed all damage right away. Also when things got stolen from garage they covered that also.

- I have never had to use them but confident they would be if needed. As far as citizens they are a solid company with a good reputation and have been around a long time and will continue to be.

Last Citizens Insurance Negative Reviews & Complaints

- This a horrible insurance company. Go somewhere else!! I called to ask a question and the mediocre representative file a claim without my permission saying that that was the only way to get a hold of an inspection. Now I have a claim on my record that is going to affect my rates forever!! And everything JUST because I had a question. Do not recommend!

- Horrible insurance. I paid it. They canceled my homeowner’s insurance after my closing and after I paid it without any notice. My insurance company bought an insurance after one year they found out I didn’t have insurance. For $10,000. Now my mortgage went out to 50% off. Horrible insurance.

- I don’t have much to add. They’re awful. Their customer service is abysmal. Their systems are terrible and shouldn’t be legal. If your agent sends them documentation, it doesn’t even notify them and then they blame you and the agent. Lol. It’s nuts. I filed a complaint with the state insurance board on them and even the insurance board used that system flaw as an excuse for them, which I found crazy.

- We were happy when we came across this home insurance. They failed to send us a letter of requirements needed, then canceled. They didn’t provide us with enough time to provide them with what was needed. Very disappointed, I don’t recommend.

- How has the state of Florida not shut down this company!! This is a absolute racket for profit. There is one home insurer in south Florida only we are mandated by mortgage banks to have insurance so the insurance company can do whatever they want. I have never filed a claim yet my policy which is catastrophic coverage only went from 3.3k to 4.1k. I have bare bones coverage. My house would have to float away to have anything covered. This can’t be legal. Where’s DeSantis!!! How about doing something governor!!

Our Fact Checking Process

What truly defines a “good” insurance company? Transparency is non-negotiable when dealing with cheap insurance.Our ratings are based on two core, non-negotiable factors:- Price Verification: All quotes presented to you are sourced directly from the current databases of licensed insurance carriers. We ensure the price is 100% accurate based on the information you provide.

- Guarantee of Independence: Our rankings and recommendations are driven by objective coverage and customer service scores, not by commissions paid by insurance companies.

- Financial Strength: We use data from independent financial ratings (such as A.M. Best or S&P) which indicate the carrier’s ability to pay out claims reliably and on time.

- Customer Experience: We analyze user reviews and complaint indexes to gauge policyholders’ satisfaction during the claim process.

Leave a Reply